교수님께서 스타벅스의 주석에서 Lease와 Asset Retirement Obligation (복구충당부채)를 분석하는 과제를 내주셔서 AICPA 시험에 합격한 뒤 오랜만에 재무회계 필기노트를 펼쳤습니다. 달달 외웠던 내용들이 1년 정도 지나니 잘 기억이 나지 않더라구요

앞으로도 꾸준히 공부를 해야 겠다는 생각이 들었습니다 ㅎㅎ

Finance/Operating Lease 구분하는 기준

1)Ownership Transfer (소유권 이전)

2)Written option to purchase + 행사할 가능성이 높을 때

3)PV of Lease payment = FV of Lease asset * 90%

4)리스 계약기간이 리스자산의 내용연수의 75% 이상

5)Specialized Lease asset (특별 주문제작)

•1년 미만의 단기 Lease 제외하고 Finance/Operating Lease는 Lessee 입장에서 동일하게 회계 처리함

•Operating Lease는 Lessee 입장에서 과거 재무상태표 상의 부채를 계상하지 않지만, 부채를 조달하는 부외금융의 효과가 있었기 때문에 현재는 Inception 시점에 ROU xx / Lease Liability xx로 동일하게 회계 처리

Finance/Operating Lease의 회계처리

Inception: ROU xx / Lease Liability xx

Payment: Interest Expense xx / Cash xx

Lease Liability (원금상환) xx

Depreciation: Amortization Expense xx / Accumulated Amortization (Or ROU 바로 Netting)

•리스 개시 시점에 인식하는 Lease Liability의 장부금액 = PV of Lease Payment

•ROU의 내용연수 기준:Lessee가 리스 자산을 계약 종료 후에 계속 사용하는지, 반납할지에 따라 결정

(1)계약기간 종료 후에 소유권 이전 or 염가매수선택권 O -> 내용연수는 리스자산의 경제적 내용연수

(2)계약기간 종료 후에 리스 제공자에게 반납 -> 내용연수는 Shorter [Lease Term, Economic Useful Life]

Finance/Operating Lease의 회계처리

•I/S상 리스부채의 이자비용을 계산하는 산식:

리스부채 기초 장부금액 * Discount Rate * M/12

•Leasehold Improvements 개념 및 회계처리

리스제공자가 리스자산에 행한 모든 종류의 자본적 지출

L.H.I의 내용연수 =Shorter [Lease Term, 경제적 내용연수]

CAPEX 지출 시점:L.H.I xx / Cash xx

Asset Retirement Obligation xx

Depreciation: Dep Exp xx / Acc. Dep xx (or L.H.I xx)

Starbucks의 Lease 자산 회계처리

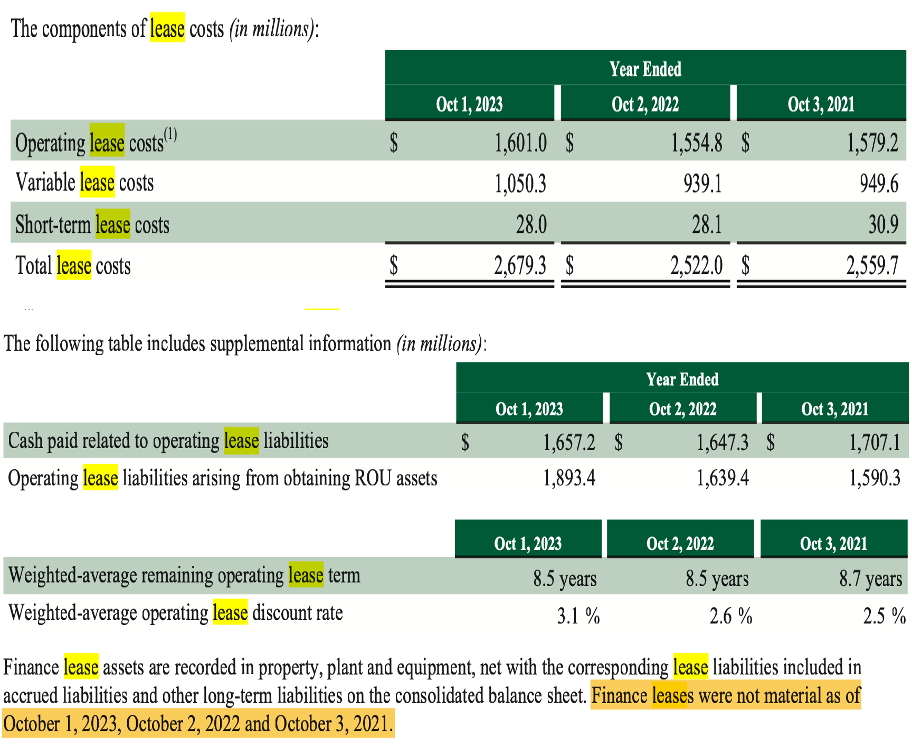

•“Majority of our leases are operating leases for our company-operated retail store locations. We also lease, among other things, roasting, distribution and warehouse facilities and office space for corporate administrative purpose.”

•”We recognize a ROU asset and lease liability for each operating and finance lease with a contractual term greater than 12 months at the time of lease inception. Our leases often include options to extend or terminate at our sole discretion, which are included in the determination of lease term when they are reasonably certain to exercise.” For the fiscal year ended Oct 3, 2021. we recognized accelerated amortization of ROU lease assets and other lease costs of $89.5 million, due to planned store closures prior to the end of contractual lease terms, which were recorded in restructuring and impairments on the consolidated statement of earnings.

•Given our policy election to combine lease and non-lease components, we also consider fixed common area maintenance part of our fixed future lease payments; therefore, fixed CAM is also included in our lease liability. Total lease costs recorded as rent and other occupancy costs include fixed operating lease costs, variable lease costs and short-term lease costs(계약기간이 12개월 이하인 단기 리스).Most of our real estate leases require we pay certain expenses, such as CAM costs, real estate taxes and other executory costs, of which fixed portion is included in operating lease costs. We recognize operating lease costs on a straight-line basis over the lease term. In addition to the above costs, variable lease costs also include amounts based on a percentage of gross sales in excess of specified levels and are recognized when probableand are not included in determining the PV of our lease liability. A significant majority of our leases are related to our company-operated stores, and their related costs are recorded within store operating expenses.

•Fixed CAM (Common area maintenance charges)의 의미: 공용구역 유지관리비

공용구역 유지관리비는 상업용 Triple Net Lease 계약에서 임차인에게 청구되는 비용 중 하나로, 임차인이 상업용 건물의 소유주에게 지불함.CAM 요금은 기본 임대료에 추가로 부과되는 비용으로, 주로 건물의 공용 공간을 임차인이 활용하고 공용 공간에 대한 유지관리비를 부담하는 것.

•Starbucks는 Landlord와 일반적으로 Triple Net Lease의 구조로 임차 계약을 체결함.

Triple Net Lease는 임대료, 부동산세, 보험료, 공공시설 사용료까지 임차인이 모두 부담하는 구조

(당사가 NNN Lease 계약을 주로 체결하는 이유는 임차인이 부동산의 유지 관리, 외관에 대한 통제권, 리스자산에 대한 보험사 등의 선택권이 Gross Lease에 비해 상대적으로 폭넓고, 기본적인 계약기간 역시 더 길게 설정할 수 있기 때문에)

당사는 최초 리스 개시 시점에 계약에 따라 리스자산에 대해 매 기간 고정적으로 지불하는 비용을 현재가치로 할인하여 재무상태표 상의 Lease Liability로 계상함. 계약에서 설정한 일정한 매출액을 초과할 경우, 추가로 임대인에게 지불하는 Variable Lease Cost는 Lease Liability의 계산에는 포함되지 않음.ROUAsset,Lease Liability의 대부분은 직영 매장과 관련되어 있으며, 이들 리스자산에 대해 발생한 비용(Total Lease Costs)은 ‘Store Operating Expenses’로 처리함.

Starbucks의 Lease 자산 회계처리

•We generally cannot determine the interest rate implicit in each of our leases. Therefore, we typically use market and term-specific incremental borrowing rates. Our incremental borrowing rate for a lease is the rate of interest we expect to pay on a collateralized basisto borrow an amount equal to the lease payments under similar terms. Because we do not borrow on a collateralized basis, we consider a combination of factors, including our credit-adjusted risk-free interest rate, the risk profile and funding cost of the specific geographic market of the lease, the lease term and the effect of adjusting the rate to reflect consideration of collateral. Our credit-adjusted risk-free rate takes into consideration interest rates we pay on our unsecured long-term bonds as well as quoted interest rate obtained from financial institutions.

•Lessee’s incremental borrowing rate의 의미:

리스 이용자가 비슷한 경제적 환경에서 비슷한 기간에 걸쳐 리스자산과 동일한 자산을 구매하기 위해

대출받았을 경우 예상되는 이자율

•증분 차입이자율을 계산하기 위해 고려해야 할 요소들:

1)리스 이용자의 신용등급

리스 이용자의 신용등급이 높을수록 더 낮은 이자율로 자금을 차입할 수 있다. 신용등급은 이자율에 직접적인 영향을 미치므로, 회사의 Credit Rating은 증분 차입이자율 계산에 중요한 요소이다

(->Credit-adjusted risk-free rate: 채무자의 신용위험을 고려하여 조정된 무 위험 수익률)

2) 리스 기간(=대출 기간)

대출 기간이 길어질수록 이자율은 상승하므로, 리스 기간이 길어질수록 증분 차입이자율은 높아진다

3) 시장 조건

경제 상황과 시중 금리 변동도 이자율 계산에 영향을 미친다

Starbucks의 Lease 자산 회계처리

•당사의 리스 계약은 주로 금융리스가 아닌 운용리스로 체결

•가중평균 잔존리스기간을 8.5년 수준으로 유지하고 있음

(2024년부터 매 년 13~14억 달러 수준의 운용리스 계약이 종료되며, 당사는 2023년 14억 달러의 리스 계약을 신규 체결)

•2023 회계연도말 장부상 운용리스 부채는 92억 달러 수준

•장기간 지속되는 고금리 상황에 당사의 증분 차입이자율은 2021년 이후 지속적으로 상승하는 추세

•중국 지역에서의 공격적인 직영점포 확장과 증분 차입이자율의 상승및 직영점 단위당 매출액 개선으로 인한 Variable lease costs의 증가에 따라 당사의 리스 관련 비용은 지속적으로 증가할 것으로 보임

Starbucks의 Lease 자산 회계처리

•The ROU asset is measured at the initial amount of the lease liability. For operating leases, ROU assets are reduced over the lease term by the recognized straight-line lease expense less the amount of accretion of the lease liability determined using the effective interest method.

ROU Asset과 Leasehold Improvements의 AmortizationExpense에 대한 정보는 현금흐름표 상의 ‘비현금성 비용의 조정’항목을 통해 알 수 있음

매 기말 14~15억 달러 수준의 Amort. Expense가 발생.B/S상 사용권자산의 장부금액은 80억 달러 안팎을 유지하고 있으나, 공격적인 매장확대 전략을 고려한다면 향후 Amort. Expenses 금액은 증가할 것이라고 전망

Asset Retirement Obligation(복구충당부채)

•미래 복구 예상비용의 현재가치를 ROU Asset의 장부금액에 가산

ROU Asset xx / A.R.O xx

•매 기말 A.R.O의 기초 장부금액에 할인율을 곱한 금액만큼 이자비용을 인식하는 회계 처리

•추후 리스 계약기간이 종료됨에 따라 리스 자산을 원상태로 복구할 때,A.R.O xx / Cash xx 회계 처리

Inception: L.H.I xx / A.R.O xx (=Estimated Fair Value of the obligation)

Depreciation: Depreciation Expense xx / Accumulated Depreciation xx(L.H.I와 동일한 Dep. Convention 사용)

Accretion: Interest Expense xx / A.R.O xx

•“Our AROs are primarily associated with leasehold improvements, which, at the end of a lease, we are contractually obligated to remove in order to comply with the lease agreement”

•“As of Oct. 1, 2023, our net ARO assets included in PPE were $25.6 million and our net ARO liabilities included in other long-term liabilities were $110.3 million.”

당사는 기존 café 형태의 매장의 renovation 및 지속적인 점포 확장 전략을 펼치고 있기 때문에 리스자산에 관련된 복구충당부채는 커질 것으로 보임. 이에 손익계산서에 인식할 감가상각비가 증가하겠지만, 기존에 인식하던 감가상각비가 매 회계기간 14억 달러 수준인 것을 감안하면 비용구조에 미치는 영향은 미미할 것으로 판단.